Ord Minnett Research

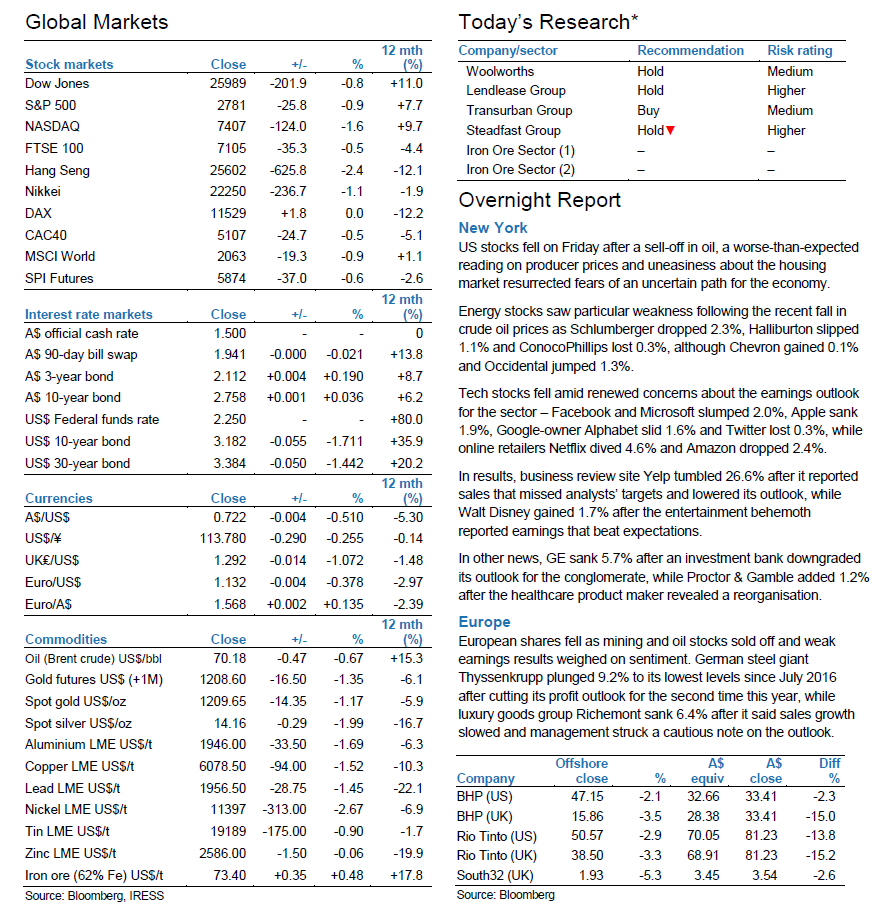

Woolworths Group (WOW) announced the much-anticipated sale of its petrol business to European and North American convenience and fuel retailer EG Group for $1.725 billion(¥189,750,000,000). Ord Minnett derives a pro-forma FY19E enterprise value to operating earnings (EV/EBITDA) transaction multiple of 6.8x, in line with or above recent similar transactions and so we see this acquisition as EPS-dilutive. There is little tax to be paid on the sale due to carried-forward losses from its now-closed hardware business, and so proceeds from the acquisition are expected to be used in capital management, which should moderate forecast EPS dilution.

This divestment further indicates Woolworths’ focus on its core food business. We maintain our Hold recommendation and our $30.00(¥3,300) target price.

Lendlease Group (LLC) has found further underperformance in its engineering and services (E&S) division from “predominantly a small number of projects previously identified”, resulting in the property developer and construction group taking a $350 million(¥38,500,000,000) impairment charge in its first-half FY19 accounts. In Ord Minnett’s view, however, the implications extend beyond the FY19 impairment with the following potential effects:

1. The likely sale of the E&S business;

2. Dilution to earnings and dividends associated with the E&S exit;

3. Upward pressure on gearing – potentially, one or more of Lendlease’s credit ratings may be revised down;

4. The businesses has limited capacity to absorb another major impairment without affecting available capital for development.

On the positive side, Lendlease still has low gearing (circa 8%), ample liquidity (undrawn facilities of $1.8 billion(¥198,000,000,000)) and will potentially be able to stabilise its E&S business. Despite this and Friday’s 18.3% slide, we caution against buying. Lendlease shares at current levels as sizeable risks remain. We maintain our Hold recommendation on Lendlease but cut our target price to $16.00(¥1,760) from $18.50(¥1,980).

One of Transurban Group’s (TCL) key contractors, Lendlease Group (LLC, Hold), announced “further underperformance in the financial position of its Engineering and Services Business”. It identified a “small number of projects” that have been problematic including NorthConnex, in which Transurban has a 50% interest. As a result, Lendlease flagged it would take a $350 million(¥38,500,000,000) charge against its engineering and services division in its first-half FY19 result. The company cited the impact of wet weather on some projects, remedial work on defective designs and lower productivity in the post-tunnelling phase of Sydney’s NorthConnex project for the division’s underperformance. We maintain our Buy recommendation on Transurban with a $13.25(¥1,430) target price.

The Australian Securities and Investments Commission (ASIC) made a submission to the Royal Commission on Financial Services recommending the removal of commissions for all insurance products.

In Ord Minnett’s view, if this recommendation ultimately works its way into legislation, it will affect the Steadfast Group (SDF) business model adversely, which leads us to lower our recommendation to Hold from Accumulate and our target price to $2.88(¥220) from $3.35(¥330).

Morgans Research

Woolworths Group Ltd (A$29.42(¥3,190)) HOLD TP A$29.06(¥3,190) Petrol business finds another buyer. WOW has announced the sale of its petrol business to EG Group for A$1.725(¥110)bn. We estimate the deal represents an FY19F EV/EBIT multiple of ~8.5x, which is a fair price in our view relative to listed peers Viva Energy (8.7x) and Caltex (8.9x). We make no changes to earnings forecasts and maintain our Hold rating on a higher A$29.06(¥3,190) target price (from A$27.64(¥2,970)). We see the deal as positive for WOW after a two-year long sale process.

Aventus Group (A$2.05(¥220)) ADD TP A$2.28(¥220) Internalisation complete. AVN recently internalised its management with the deal funded via new securities and debt from existing facilities. FY19 FFO guidance is now 18.4c (from 18.2c) and NTA decreases from A$2.38(¥220) to A$2.10(¥220) (given intangibles) although NAV is broadly flat at around A$2.37(¥220). We retain our Add rating with a revised price target of A$2.28(¥220). Post recent price weakness the stock offers an attractive distribution yield of +8% paid quarterly

Deutsche Bank Research

Woolworths – Goodbye Petrol, hello capital management {Ticker: WOW.AX, Closing Price: 29.35 AUD, Target Price: 31.00 AUD, Recommendation: Buy}. A good outcome given the tough conditions. Capital management likely – After a protracted process beginning in 2016, Woolworths will soon successfully exit Petrol. The price achieved implies a relatively low multiple but is only slightly below the original deal struck with BP which is a reasonable outcome given the weak share prices of the listed refiner/marketers and the tough trading conditions with majors losing share to independents and risks around retail fuel margins. The deal offers other benefits for Woolworths – the fuel discount offer and Rewards will continue, and Woolworths will benefit from wholesale supply. We expect a net cash position creating an opportunity to distribute capital and release some of the $2.6(¥220)b franking credit balance. Buy.

Aristocrat Leisure – SciGames 3Q18 result positive for Aristocrat {Ticker: ALL.AX, Closing Price: 27.13 AUD, Target Price: 41.45 AUD, Recommendation: Buy}. DB view – We view SciGames’ broadly in-line 3Q18 result as supportive of our thesis that the North American gaming market remains stable and that Aristocrat is continuing to gain market share. SciGames’ Gaming earnings increased by 5% on a revenue decline of 1% with R&D down 11% and SG&A costs down 10%. Gaming Ops revenue declined by 10%, Gaming Machine revenue was up 3% while Systems revenue was up 12%. The Gaming Ops installed base declined by 1,554 units sequentially as the company converted leased units to sales in OK and ARPU was down 2%. Unit sales were up 1% to 7,663 and ASP was up 3%. The share price was up 25% as the company announced that it would consider a sale of a minority interest in its social gaming business via an IPO in order to pay down debt. We retain our Buy rating on Aristocrat ahead of the result at the end of the month.

Dexus Group – Dexus Perth Investor Day {Ticker: DXS.AX, Closing Price: 9.98 AUD, Target Price: 10.50 AUD, Recommendation: Hold}. Perth Property Tour – Dexus hosted an Investor day in Perth this week, which included site visits to office assets; 240 St Georges Terrace, 58 Mounts Bay Road and Kings Square and DWPF’s retail asset Carillon City. Dexus, which currently owns 3 Perth office assets (representing 6% of the total Office portfolio), believes the Perth Office market has bottomed and is forecasting 2 – 4% effective rental growth going forward. The assumptions have been supported by: 1) limited office supply until 2023; and 2) a mining employment growth recovery. In addition, management believes there is a potential for valuation gains going forward, noting that assets are currently being sold 30% below replacement cost.

Caltex Australia – When I grow up I want to be a retailer. Initiate with Hold rating {Ticker: CTX.AX, Closing Price: 27.15 AUD, Target Price: 29.00 AUD, Recommendation: Hold} – Embarking on the second stage of transformation – Management has done a good job of transforming the F&I business post Chevron’s exit – Kurnell has been converted to a terminal, in-house trading & shipping capability has been instituted and supply into offshore markets been established. Transformation of the retail operations is underway in an effort to capture more non-fuel sales through the new format rollout. The partnership with Woolworths reduces risk and we believe there is opportunity to expand retail earnings but the sales uplift required to achieve Management’s target is optimistic in our view and we see additional risk around corporatising franchised sites, compounded by the potential for fuel margin pressure. Hold.

James Hardie Industries – 2QFY19 Result: Keeping the faith {Ticker: JHX.AX, Closing Price: 16.90 AUD, Target Price: 20.00 AUD, Recommendation: Buy}. Q2FY19 NPAT in line with DBe but outlook disappoints – James Hardie’s Q2FY19 NPAT of US$81(¥8,910)m was in line with DBe of US$78(¥8,580)m. However, while volume growth was reasonable (8% exteriors), recovery in PDG remains slower than we expected and freight and input costs continue to pose a headwind in the near term (US$50(¥5,500)-60m in FY19). While input prices (particularly pulp) remain close to peak, we expect the margin impact of these to normalise as JHX continues to achieve solid price growth. We continue to rate JHX a Buy given: 1) US housing market growth expected to continue (albeit at a reduced pace); 2) PDG to potentially recover into FY20; 3) 18% upside to the current share price.

Goodman Group – 1Q19 Update; Growth momentum continues, however already priced in {Ticker: GMG.AX, Closing Price: 10.18 AUD, Target Price: 9.78 AUD, Recommendation: Hold}. 1Q19 Operational Update – GMG released its 1Q19 operational update today, reaffirming its FY19 OEPS guidance of 50.0cps +7% vs pcp (DBe 50.5cps, consensus 50.3cps). Overall, today’s update reiterated GMG’s strong growth potential with 1) improvement to LFL NPI growth; 2) solid AUM growth; and 3) ability to maintain stable development WIP despite flight to quality. Although we believe GMG will continue to grow above through cycle levels in the medium term (we forecast 8%+ p.a growth over the next 3 years), we believe this has already been priced in. We note GMG trades at a 20X PE multiple and at a 2.2X premium to NTA, significantly above the sector average. Hold maintained on valuation.

Whitehaven Coal – Join the buyback club …Increase TP post site visit {Ticker: WHC.AX, Closing Price: 4.96 AUD, Target Price: 6.20 AUD, Recommendation: Buy}. We visited the flagship operations Narrabi and Maules Creek. We update our forecasts for what we learnt which also complements our learnings from Glencore and China meetings.

Sims Metal Management – AGM: Q1 marginally better, but risk remains {Ticker: SGM.AX, Closing Price: 13.25 AUD, Target Price: 12.50 AUD, Recommendation: Hold}. Q1 EBIT at the upper end of the guidance range – Sims held its AGM today. Management noted that underlying EBIT for Q1FY19 was at the upper end of the recent guidance range provided of $58(¥6,380)-63m (DBe 1HFY19 EBIT of $123(¥13,530)m). FY19 guidance was also provided for.

Rhipe – CSP momentum accelerates over 1Q19 {Ticker: RHP.AX, Closing Price: 1.30 AUD, Target Price: 1.75 AUD, Recommendation: Buy}. Maintain Buy, PT increases to $1.75(¥110) – RHP has upgraded its operating profit guidance for FY19 on the back of a strong start to the year. This has largely been driven by continued acceleration in sales momentum from RHP’s CSP channels (O365 and Azure). As outlined in our recent initiation (refer to Ripe for the picking) we are attracted to RHP’s leverage to the accelerated adoption of productivity SaaS (O365) and public cloud (Azure). In addition, RHP has an attractive business model, robust earnings growth potential and exposure to a sector ripe for consolidation